Nusantara Sawit Sejahtera

Plantation | Fundamental Price : 1,609

Major Assumption

WACC : 7.27% | TGR : 5% | CAPM : 9.38%

- 1.5% Planted area / year

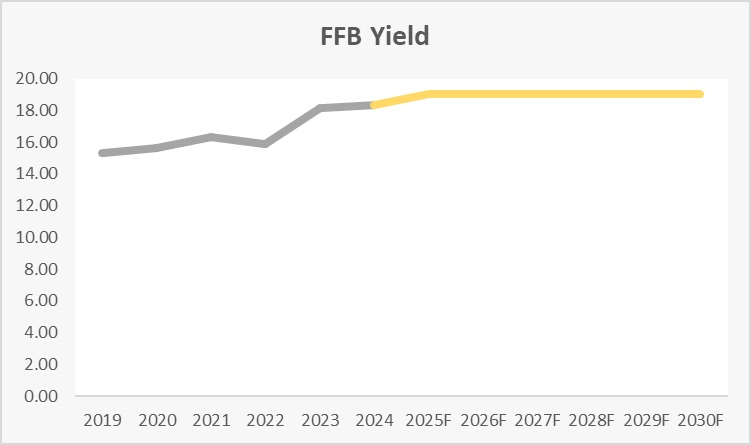

- Yield peaked at 19/ha

- ASP -4% than market

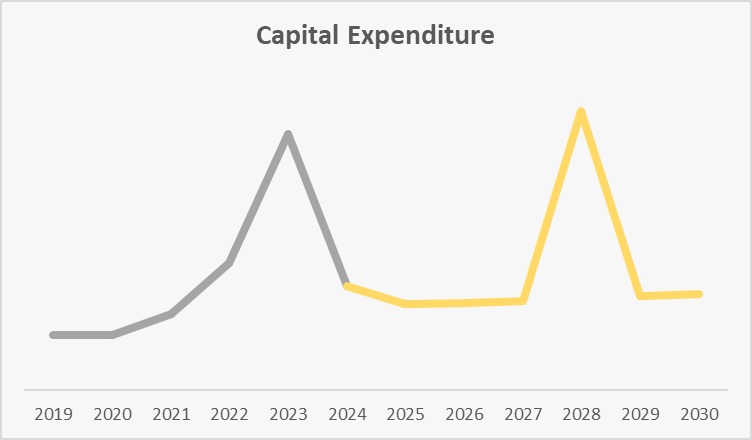

- + 1 Mills at IDR 250bn Capex (2028)

Potential & Downside

- Strong Fundamental & Price upwards

- Mature Plantation (Clear expansion)

- Downside: Import levy spillover, Price falls

Brief Analysis

Indonesia's CPO sector outlook suggests broadly stable production supported by maturing plantation areas and modest new planting. Structurally, Indonesian CPO remains price-discounted to Malaysia, and recent inventory overhang in Malaysia has intensified price competition.

Within this context, NSSS is positioned in a prime maturity phase. Its direct pipeline logistics system mainly stabilizes cost per ton, protecting margins. Financial projections assume conservative yields, yet still imply solid earnings sensitivity, supporting a BUY/accumulate stance.

Operational & Production Outlook

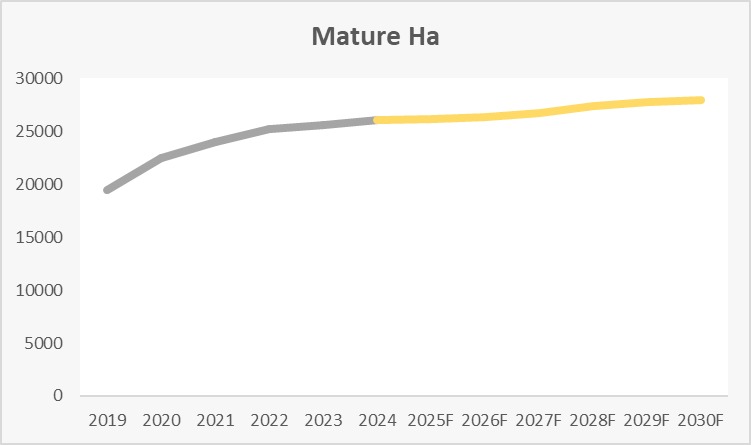

As we know, the cycle for CPO lasts for 20 years before it runs out of yield. From 2019 to 2024, Nusantara Sawit are increasing their mature Ha from 4-6 years cycle of FFB plantation so that from 2025 onwards, those plantation are going to be ready for production.

We can see that the mature area is approaching its all time high with a constant yield of prime age 19 ton per Ha. These indicators backed the previous revenue graph and shows the rationale behind the massive increase.

Capex & Leverage

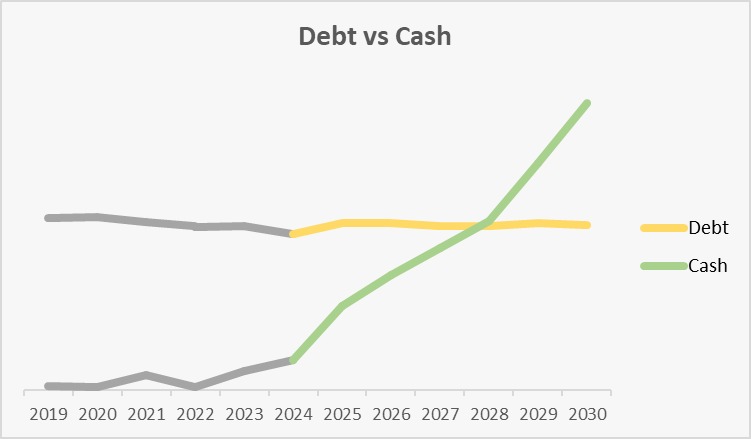

From capital expenditure position, their only spending are limited to opening new mills to process the yield and most of it are funded from cash payment rather than debt. Plantation business does not require capital expenditure except investing for mills and pipe, and only slight amount for maintenance of fixed assets. From leverage and liquidity scope, they are projected to have a constant debt while stocking pile of cash from increase in revenue. As we know, Nusantara Sawit might announce more movement in the next window dressing as to maintain their prime yield or acquiring to increase their yield.

Recommendation

With indicators showing an exponentially increasing numbers for the next several years, my call on Nusantara Sawit extents to buy and buy more when the price is cheaper as Nusantara Sawit shows a premium towards its peer due to prime age of production.