Medco Energi Internasional

Oil & Gas Upstream | Fundamental Price : Rp 3.154 - Rp 7.915

Major Assumption

WACC : 10% | TGR : 3%

- 3 Acquisition scheme (2028, 2031, 2034) at 400mil capex & split 1/2 cash payment

- Oil prices at 68 (Brent) and 3% implied discount

- Gas Index at 29% and fixed at 71%

Valuation Summary

-

DCF Valuation: Rp 7.915 / Share

Implied 9.6x Forward EV/EBITDA -

Relative Valuation: Rp 3.154 / Share

Peers EV/EBITDA 4.6x & 2027 EBITDA USD 1.42b

Potential & Downside

- Potential: Oil Price goes up

- Potential: Successful Acquisitions

- Downside: Supply disruptions from war

Brief Analysis

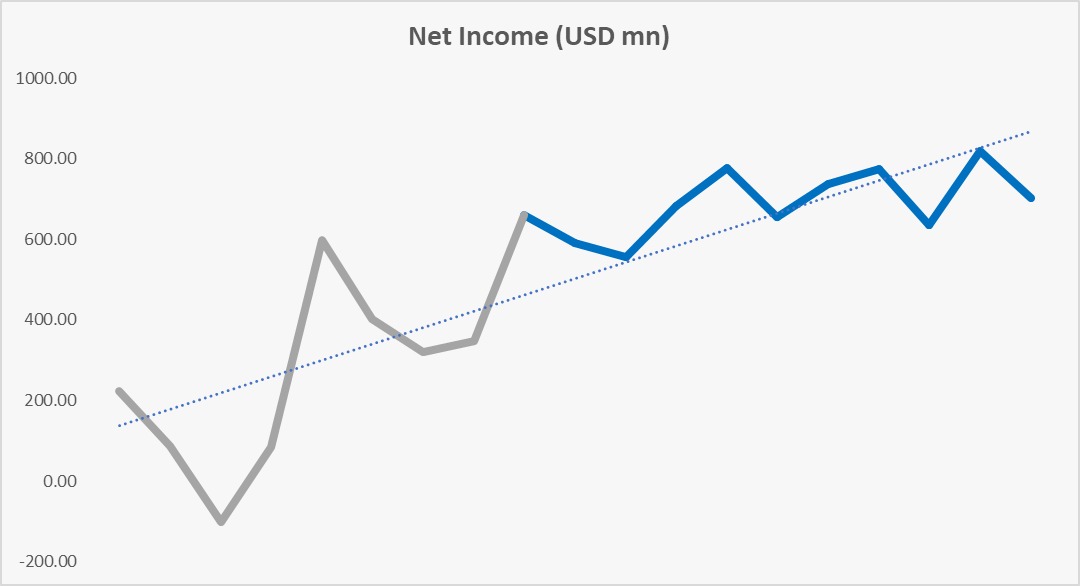

With assumption being carried out on oil price remain stable between 65 and 70, this model include prices that did not take into consideration the price spikes due to supply restrictions of war. If so, the revenue would be exponentially larger with all cost remain constant as the factor would only be external which is prices.

MedcoEnergi is one of the limited upstream players in Indonesia’s oil & gas landscape with MEDC being premium to others. The price history is more stable in the timeframe of two to three years, and less volatile towards outflow and inflow (Ex: MSCI January 2026).

Business Model & Reserve Management

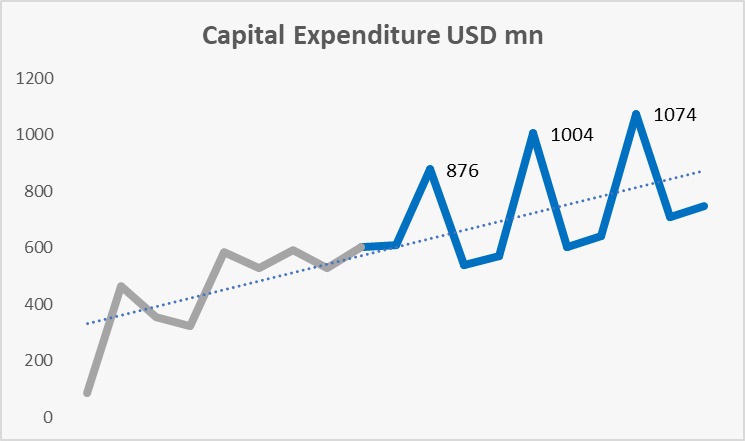

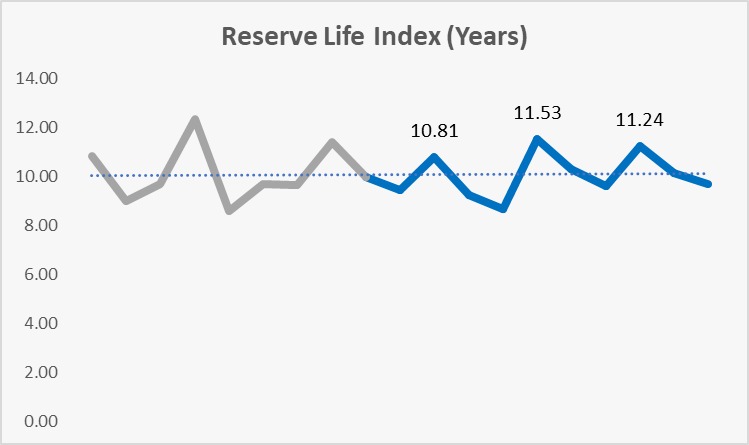

With assumption based on the coordination with the company itself, i built the assumption on the understanding that MEDC has turned its business model more similar towards venture capital. From 2017 to 2025, five acquisitions were done to maintain a cycle of peak production while maintaining reserve life index (RLI). From 2026 onwards, three acquisitions were model as their way on sustaining the business.

Those acquisitions are indicated by 3 peaked in capital expenditures. Those acquisitions are mostly new oil and gas reserves from blocks and corridors. Furthermore, those acquisitions were also assumed to add their contingency reserve (2C) which in the window dressing year without any acquisition, were transformed to a 2P reserve at $0.70 per boe hence it can be seen that capital expenditure are still higher compared to historical year because on top of maintenance cost, they also add a conversion cost to increase their reserve.

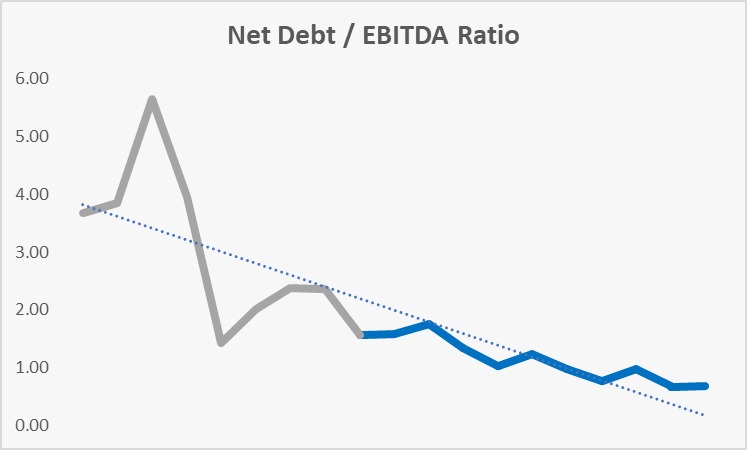

Leverage & Acquisition Financing

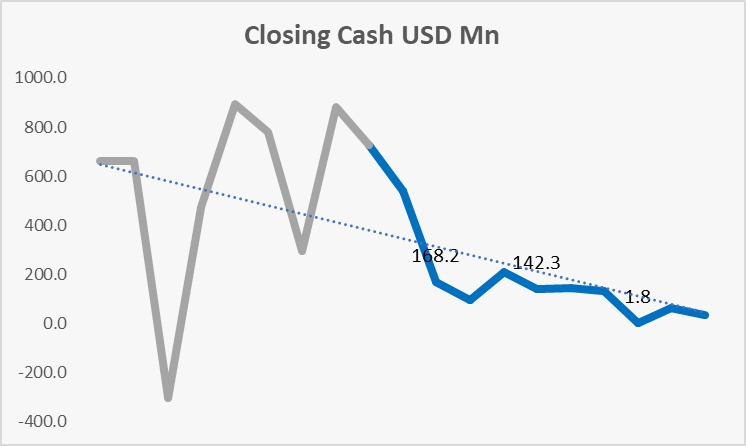

With their acquisitions be based on debt financing, the assumptions were based on half split financing from cash and debt. The debt itself are to be repaid in 36 to 48 months with revolving credit facilities to maintain positive cash.

As we can see, MEDC is projected to have a declining Net Debt to EBITDA. This ratios shows that while Net Debt is assumed to on the same level each year from constant acquisition payment, EBITDA is increasing as the acquisition have become a productive assets.

Investment Thesis & Recommendation

As those productivity and leverage number shows, It is quite reasonable to model MedcoEnergi on a bullish basis as oil price supports the movement. If we only account after 2018 which MEDC is being restructured, it can be seen that they are shaping the foundation of the business model towards a more sustainable model but yet still productive enough to become nation’s biggest private upstream player in oil and gas.

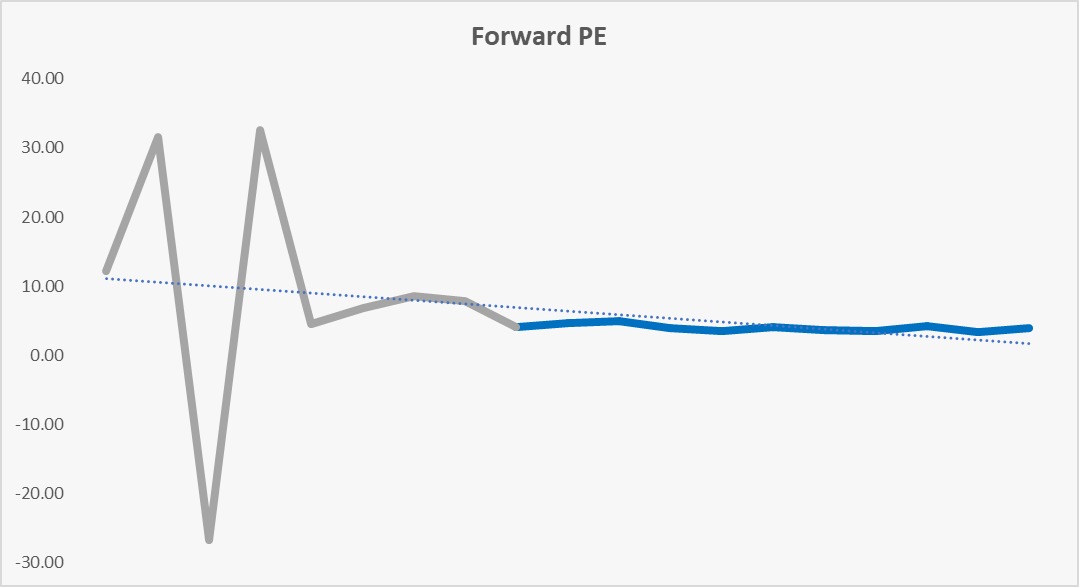

With increasing revenue stream, heathy reserve life index, healthy leverage indicators from net debt, all while having a target of Price Earning Ratio stabling throughout the period, my call on MEDC is not limited beyond the upcoming of oil price but a foundation that a portfolio needs to have to maintain its alpha.